A Systematic Review: Theoretical Perspective of Integrated Reporting and Corporate Disclosure

Keywords:

Integrated reporting, institutional theory, legitimacy theory, agency theory, corporate disclosureAbstract

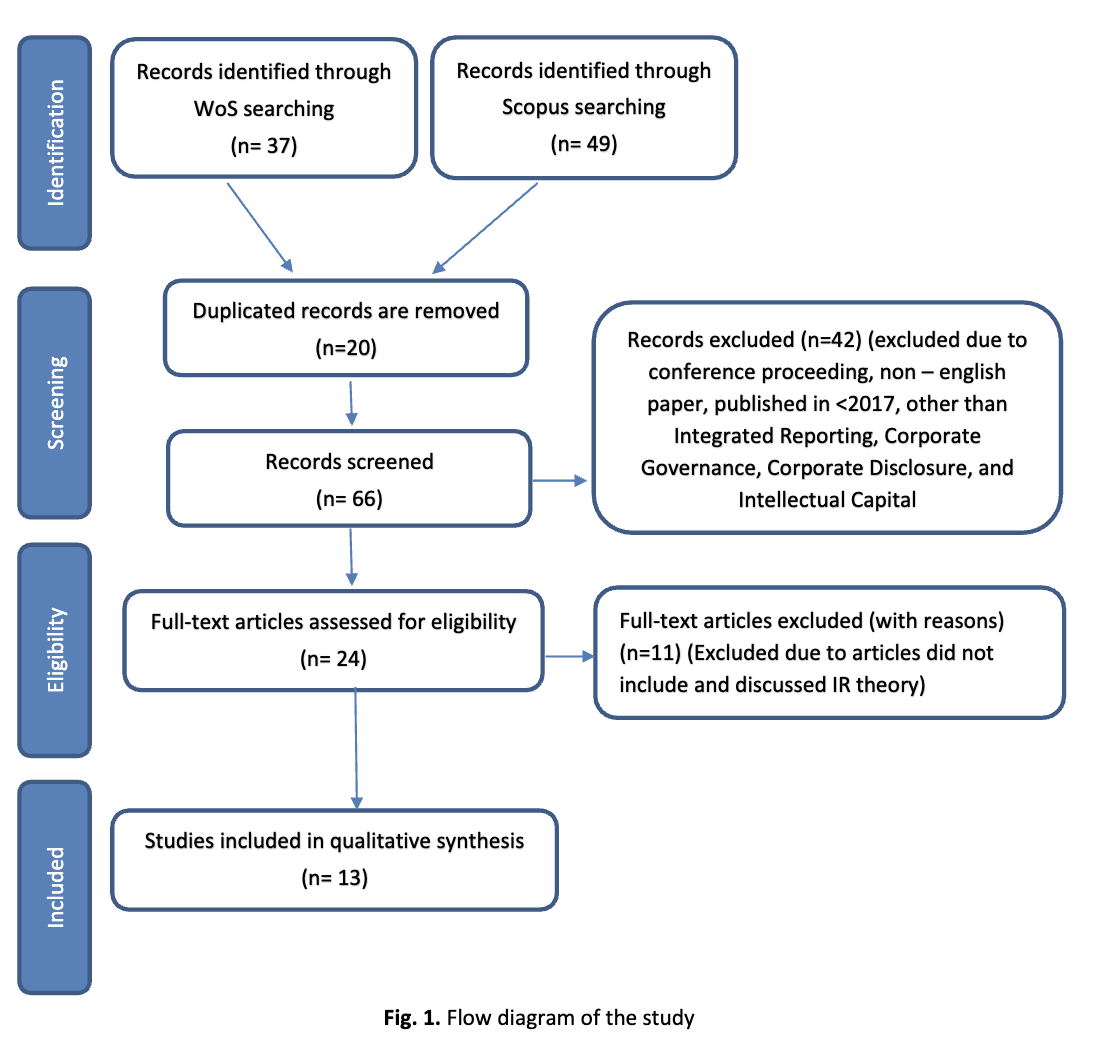

This paper aims to systematically review published articles on the underpinning theories that contribute to corporate disclosure in Integrated Reports (IR). This study adopted Preferred Reporting Items for Systematic Review and Meta-Analyses (PRISMA) to review published journals by utilizing Scopus and Web of Science as the two primary journal databases. 13 related articles were reviewed. Further review of these articles resulted in five main themes – Agency theory, Signaling theory, Legitimacy theory, Stakeholder theory, and Institutional theory. These five themes further produced a total of 13 sub-themes. Recommendation for future studies should explore more searching techniques such as citation tracking, reference searching, snowballing and contacting experts. These findings will assist policymakers, international bodies, and researchers to further extend the current literature.